In 2012, 46% of Americans carried over a credit card balance from month to month. For those households with credit card debt, the average balance of that debt was an astonishing $15,800. Why do people have so much debt and why can they not pay off their balances?

You generally fall into two categories if you have debt, whether it’s credit card debt or any other debt for that matter. There are those who simply don’t care about the amount they spend and have no concern for the fact that their monthly expenses are greater than the amount they bring in. On the other hand, some people create budgets and conscientiously try to pay off debt each month.

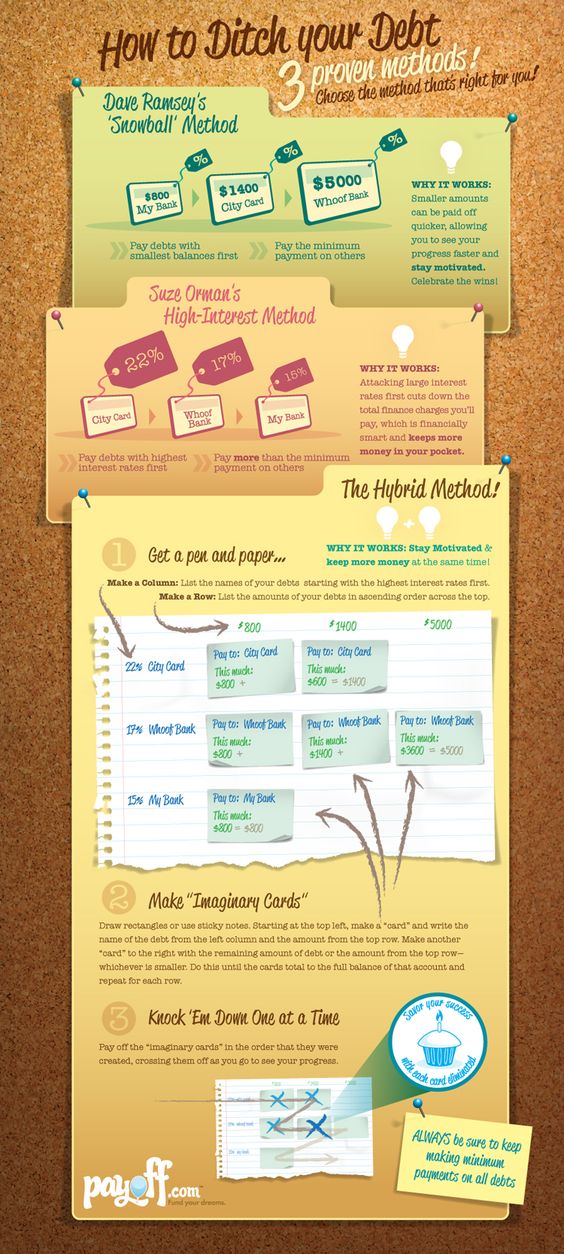

If you’re in the first category, I can’t help you. Someday, you will wake up and come to the realization that you cannot continue in that manner, but nothing people say will be the catalyst for change. However, if you make the habit of paying more than your minimum payments each month and you’d like to be debt free, today’s infographic may help.

Most of us know that making the minimum monthly payment is a fools’ way to pay off debt. It will take years and years of $50 payments to pay off your principal and all of the interest. You could and should pay more than the minimum amount due, but which loan to concentrate on first is not always a simple question to answer.

Two popular methods today for prioritizing debt payments are Dave Ramsey’s ‘snowball’ effect and Suze Orman’s high-interest method. A third and less talked about strategy is to combine the two. All three methods will produce a debt free outcome much faster than paying the measly minimum payment.

Both the Ramsey method and the Orman method will have a debt of $7,200 paid off within 14 months, but the Ramsey method will have you paying slightly more in interest ($757 vs $736). The only time this method is preferred is when you need a little motivation to continue paying more than the minimum due each month. Sometimes it’s also easier and simplifies things to make payments to fewer loans.

If you’re not sure which method is right for you, choose a combination of both.

Finally, people pay off large amounts of debt all the time. For example Brock over at CleverDude.com is in the process of eliminating $10,000 worth of debt, and James at thousandaire.com was able to pay off $40,000 worth of debt. So, it can be done.

Need more help getting out of debt? Check out these articles.

Can Debt Settlement Be Your Way Out of Debt?

How to Prioritize Debt Payments

How to Manage Debt in Your Marriage

Readers: Who has used one of these three methods and benefited from the results? Who was making minimum payments but is now motivated to develop a plan to become debt free using one of these payoff methods?